Cash Flow for Solopreneurs: A Simple System

Your Stripe notification reads "$5,000 received." Your bank balance reads $212. Both are true at the same time, and that contradiction is the entire problem.

Most solopreneurs do not need a bigger finance stack. They need a money routine they can actually repeat: split incoming cash, protect taxes, decide what is safe to spend, and pay themselves without creating next month's problem.

Why solopreneurs need a money operating system

For a solopreneur, cash flow is simpler than the jargon makes it sound: what has already cleared, what must go out next, and what is still safe to use after taxes and obligations. If you want the terminology, keep the Cash Flow Glossary nearby. This guide is about the operating system.

Five structural patterns commonly drain solopreneur liquidity. Many solopreneurs face several of these at once:

In the typical community, 29 percent of small businesses were unprofitable, and 47 percent had two weeks or less of cash liquidity.

Quick start: 3 steps to take today

- Separate accounts. One business checking, one tax savings.

- Split every deposit. Fixed percentage to taxes and reserve before you spend.

- Check the next 14 days. Cleared operating cash minus upcoming obligations, any tax funding gap, and your protected buffer = safe-to-spend.

Why solopreneurs can earn well and still feel cash-poor

A solopreneur can show profit on paper while staring at an empty bank account because accounts receivable — money owed to you — has not converted into actual dollars, while cash outflows have already happened.

-

Accrual accounting recognizes revenue when you earn it, even before the client pays.

-

Cash accounting recognizes revenue when money hits the bank.

-

The gap between those two moments is the timing mismatch. That is where cash crunches happen.

Under the cash method, you generally report income in the tax year you receive it, and deduct expenses in the tax year in which you pay the expenses.

Under the accrual method, you generally report income in the tax year you earn it, regardless of when payment is received.

Timing mismatch is the most common culprit, but it is not the only one. Cash can also get squeezed by things that reduce bank balance without reducing profit the same way, or at the same time: paying down debt principal, buying equipment (CapEx), inventory purchases, credit card "float" (spend now, cash leaves later), and taxes.

Timing mismatch example: the payout that arrives after the bills are due

A solopreneur sells $8,000 worth of digital products in early January through an online marketplace. The platform holds funds for review and pays out on a 14-day rolling schedule. But the bills do not wait:

- Hosting and tools:

$600due January 5 - Contractor:

$1,500due January 10 - Ad spend:

$2,000due January 15

Total outflows by mid-month: $4,100. If the starting bank balance sits below that, the solopreneur is short before the first payout clears. Revenue is strong. Cash is missing.

Why solopreneurs are more vulnerable than "regular" businesses

Solopreneurs operate without the cushions larger companies take for granted. There is no one watching cash timing for you, no predictable cadence that smooths inflows, and often no buffer to absorb a slow week. One late client payment can cascade into missed bills.

Time is the real constraint. If the system takes an hour and five logins to update, it will not survive your busiest weeks.

So the rest of this guide sticks to two habits: a simple allocation rule you run on every deposit, and a short weekly ritual that keeps you ahead of the cash trough.

The simplest cash flow framework: cash in, cash out, cash on hand

A practical cash system comes down to one equation and a handful of categories. The payoff is control over your ending cash balance and a measurable cash runway, the number of weeks your business survives on current reserves.

- Beginning cash balance — what you start with.

- Cash in (inflows) — money that actually hits the bank.

- Cash out (outflows) — money that leaves.

- Ending cash balance — what remains.

- Cash runway — how long that balance lasts at your current burn rate.

The core formula worth memorizing

Ending Cash = Beginning Cash + Cash Inflows − Cash Outflows

Cash Runway = Cash on Hand / Average Weekly Net Outflow (cash burn)

Note: This runway math only applies when your average weekly net outflow is positive, meaning you are "burning" cash. If inflows are consistently greater than outflows, runway is not the constraint.

If your weekly net outflow averages $1,000 and you hold $4,000 in the bank, your runway is four weeks. Ideally, it should not surprise you.

The minimum categories to track

Track categories that change decisions. Too much detail creates friction and kills the weekly habit. Rule of thumb: if a category does not change what you do, merge it into a broader one.

Inflow categories:

- Client payments (cleared)

- Product / digital sales (cleared)

- Owner contributions (cash injected by you)

Critical counting rule for this workflow: Treat money as spendable cash only when it clears your bank. Not when invoiced. Not when promised. Still track invoices separately so you can forecast realistically.

Outflow categories:

- Owner pay / draw

- Taxes (keep as a separate line)

- Rent / coworking

- Software / SaaS

- Contractors / freelancers

- Marketing / ads

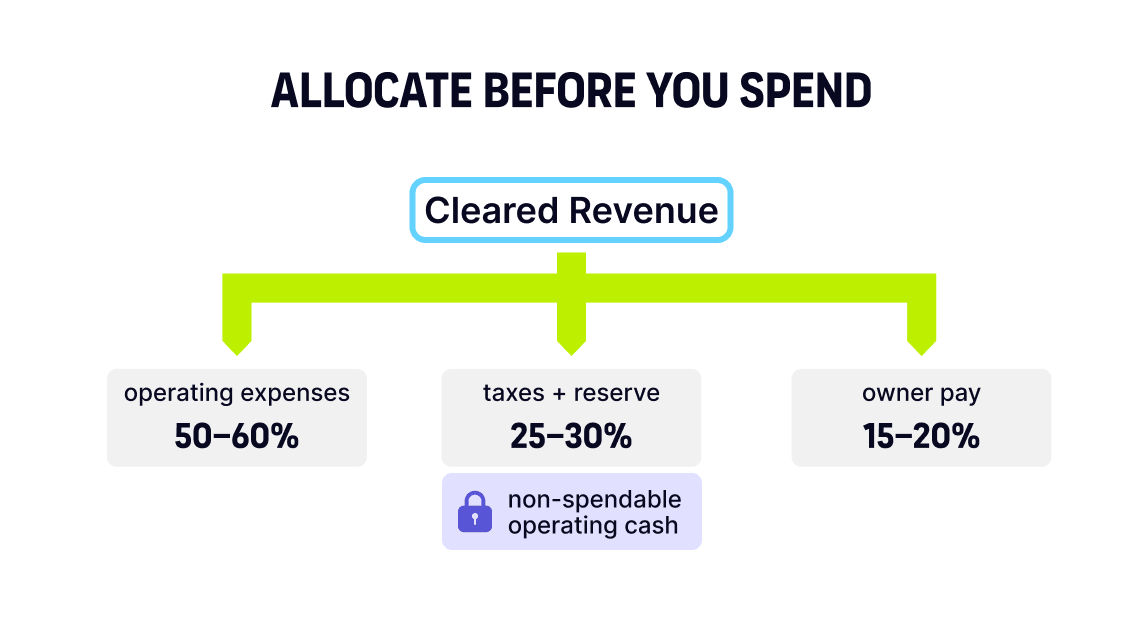

The "3 buckets" setup: a 15-minute system that reduces cash crunch risk

The point is to allocate before you spend. Every dollar that enters the business gets split into three buckets: operating expenses, taxes + reserve, and owner pay, before you start paying bills.

- Revenue lands in the business checking account.

- An automatic, or manual, percentage split sends portions to subaccounts.

- The taxes + reserve bucket is treated as ring-fenced cash: you pay taxes from it when they are due, and whatever remains functions as your reserve.

Separate business and personal finances

If personal and business money share one account, your categories and your cash balance get blurry fast. Separate the accounts first. If privacy is a concern, an offline-first approach to financial data is worth considering.

As soon as you start accepting or spending money as your business, you should open a business bank account.

Open today:

- Dedicated business checking account

- Separate business debit or credit card

- Separate savings account for taxes and reserve

Profit First-Lite: the solopreneur bucket system

Starting allocation ranges, adjusted after 4 to 6 weeks of real data:

Important: These are starting ranges, not rules. The right split depends on your margins, fixed costs, debt, and your real effective tax rate.

| Bucket | Starting range | Purpose |

|---|---|---|

| Operating expenses | 50-60% | Rent, tools, contractors, marketing |

| Taxes + reserve | 25-30% | Estimated taxes + a safety buffer |

| Owner pay | 15-20% | Your compensation (baseline + bonus) |

Pick one number in each row so your final split still adds up to 100%.

Know your financial floor: the minimum monthly obligation required to avoid missing essential commitments: fixed costs plus required payments.

Separating funds into distinct buckets makes accidental spending much harder. When taxes and owner pay are separated, you stop negotiating with yourself every time a deposit arrives.

Automations that remove willpower from the equation

Do not rely on willpower. Automate the boring parts:

- Auto-transfers into subaccounts on every deposit

- If your bank cannot split per deposit, do a weekly "sweep" transfer right after your cash review

- Invoice reminders sent automatically on a schedule

- Recurring bills on autopay, but only for predictable bills you can cover

- Calendar alerts for estimated-tax due dates in your jurisdiction

Build your 13-week cash flow forecast

The bucket system tells you WHERE money sits right now. The forecast tells you WHEN it moves. Together they form the complete picture.

For the full spreadsheet layout, formulas, and weekly update ritual, use the 13-Week Cash Flow Forecast: Template & Guide. Below is the solopreneur quick-start.

Before you build, gather three things:

- Current bank balance — cleared funds in your Operating account

- What is owed to you — invoice amounts and realistic paid dates

- What you owe — due dates and amounts, including owner pay, taxes, and annual renewals

Then project 13 weeks forward: expected inflows by week, expected outflows by week, and Opening + Inflows − Outflows = Closing for each column. The week with the lowest balance is your cash trough — the week that forces painful choices, unless you see it early.

Mini-example: spotting the trough

| Metric | Week 1 | Week 2 | Week 3 | Week 4 |

|---|---|---|---|---|

| Beginning cash | $4,000 | $3,500 | $1,500 | $100 |

| Expected inflows | $500 | $0 | $600 | $5,000 |

| Expected outflows | $1,000 | $2,000 (Rent) | $2,000 (Taxes) | $800 |

| Ending cash | $3,500 | $1,500 | $100 (Trough) | $4,300 |

If the Week 3 tax payment is not actually due until Week 4, move the forecasted tax outflow to Week 4. If it is due in Week 3, accelerate collections, cut non-essential spending, or talk to a tax professional early.

Irregular income and marketplace payouts

Solopreneur income spikes, dips, and clusters. Anchor the current week to cleared cash and future weeks to conservative settlement dates. Invoices, pending payouts, and optimistic promises are not spendable money yet. For credit cards, forecast the cash-out on the statement payment due date.

Every platform has its own payout schedule and settlement delay. Map each platform's settlement window and use conservative payout dates in your forecast. Never schedule bills against unsettled payouts.

The weekly forecast catches near-term crises. For the deeper strategy view — methods, models, and common mistakes — see What Is a Cash Flow Forecast?.

Your weekly cash dashboard: one page, 7 numbers, 20 minutes

Seven numbers are enough. Put them on one page. Spend 20 minutes with them each Monday, and the rest of the week gets calmer.

| Metric | Example | Rule |

|---|---|---|

| Cash on hand | $8,640 | Cleared operating cash only |

| Mandatory payments due (14 days) | $3,210 | Must-pay bills before the next two reviews |

| Taxes reserved | $2,150 | Tax cash already set aside |

| Reserve runway (weeks) | 7.2 | Protected buffer / average mandatory weekly outflows |

| Expected inflows (14 days) | $4,020 | Planning only, not spendable yet |

| Overdue invoices | $1,180 | Follow-up list, not guaranteed cash |

| Safe-to-spend this week | $1,390 | Discretionary spending ceiling |

Use two rules, then apply them to the numbers above:

Safe-to-spend = cleared operating cash − mandatory payments due − tax funding gap − protected bufferReserve runway = protected buffer / average mandatory weekly outflowsSafe-to-spend = $8,640 operating cash − $3,210 − $0 − $4,040 = $1,390Reserve runway = $4,040 / $560 = 7.2 weeks

At 7.2 weeks, the reserve is above the 3-week floor but below the 8-12-week comfort range.

Resolving the reserve target: minimums vs. comfort

Holding the right amount of cash is a tradeoff: safety vs. opportunity cost. Here is a practical starting point. Adjust for seasonality, client concentration, and how fast you can realistically collect.

-

Absolute minimum (survival).

3weeks of mandatory cash outflows. If you drop below this, halt all non-essential spending. -

Comfort target (health).

8to12weeks of mandatory cash outflows. If your income is lumpy or client-concentrated,3months is a reasonable target.

The 20-minute weekly cash review ritual

Six steps. Same order every week. Put it on autopilot.

- 1

Open the bank

Reconcile last week's cleared transactions.

- 2

Update the metrics

Update the numbers in your spreadsheet or app.

- 3

Map obligations

List what is due before the next expected inflow.

- 4

Pick 1-2 collection actions

Choose one or two actions to accelerate inflows, such as a collection call or a follow-up email.

- 5

Execute bucket transfers

Move money if deposits arrived since the last review.

- 6

Set the safe-to-spend limit

Define the number for the coming week.

Book a recurring calendar block for this review. Same day. Same time. Every week. Skipped reviews degrade forecast accuracy and bring back the financial anxiety the system was built to eliminate.

If maintaining this ritual in a spreadsheet creates friction, a lightweight tool like onbalance tracks the same forward view with less manual upkeep.

Pay yourself without the guilt: two modes that work

Owner compensation is a cash flow design decision. Overpay yourself, and tax payments get squeezed later. Underpay yourself, and you risk burnout and resentment toward the business.

Note: If you run payroll, for example because you are taxed as an S-corp, owner pay mechanics can differ: salary vs. distributions. Align your pay structure with a qualified tax pro.

Mode 1: the fixed "salary" baseline

Set a minimum owner pay baseline: the amount required to cover personal essentials. Treat it as a mandatory outflow, paid on a fixed schedule, just like rent.

Mode 2: the bonus, only when the system says yes

A bonus is earned when all four conditions are true at the same time:

- Taxes are funded for the relevant period.

- Reserve meets the absolute minimum runway target (

>= 3weeks). - There are no overdue payables.

- The forecast shows non-negative ending cash across the near horizon.

If any condition fails, the surplus stays in reserve.

Tight cash weeks: protect the system before you improvise

When cash gets tight, the first job is not to invent new revenue. It is to protect the money system: taxes funded, reserve intact, and owner pay realistic.

Protect the floor first

Before changing anything else, check three numbers: the tax funding gap, mandatory bills due in the next 30 days, and minimum reserve runway. If one of those is underfunded, move cash there first. Pause extra owner draws until the near-term forecast is back above zero.

Cut discretionary spend before core capacity

Use the fat / muscle / bone filter, but apply it to your own operation. Cut unused software, optional subscriptions, and low-return spending first. Delay equipment upgrades, experiments, or non-essential hires that do not protect near-term delivery.

Use credit only as a bridge, not a budget

If you need temporary financing, model the repayment in the same forecast before you use it. Credit can smooth timing. It should never become your safe-to-spend number.

If the real problem is late invoices, deposits, milestone billing, or collections follow-up, use a collections-focused playbook rather than adding more bucket rules.

Taxes and cash flow: make tax money untouchable

One operating rule: tax cash leaves Operating the same day revenue clears. Move a fixed percentage of every payment into Taxes + Reserve. If you collect sales tax or VAT, move it out immediately. In many jurisdictions those collections function as remittance funds, not discretionary operating cash.

Taxes must be paid as you earn or receive income during the year, either through withholding or estimated tax payments.

The exact rate depends on your jurisdiction, structure, and income level. For the full sinking fund method and quarterly payment schedule, see Taxes Without Surprises in Cash Flow for Freelancers.

6 cash flow traps that catch even experienced solopreneurs

- Subscription creep. Tools accumulate silently. Run a monthly audit and cancel anything unused in the last

30days. - Client concentration. If one client drives most of the revenue, increase your reserve runway and shorten that client's payment terms.

- Discounting without cash modeling. A 10% discount changes margin. A 10% discount with

Net 60terms changes cash timing for months. Model both. - Ignoring aging receivables. Review open invoices weekly. Escalate at

7days overdue, not30. For a full collections sequence, see Cash Flow for Freelancers. - Buying equipment without a forecast. A

$3,000purchase is not just an outflow — forecast the recovery period and the weeks of reduced runway. - No plan for seasonal dips. Revenue dips are predictable with a year of data. Build reserves in peak months to cover the trough.

Best cash flow tools: choose the lightest system you will actually review

For a solopreneur, the tool's job is simple: show cleared cash, upcoming obligations, tax and reserve balances, and safe-to-spend without turning money into admin work.

What the tool must support

A simple upgrade path

-

Spreadsheet first. Fine when transaction volume is low and you will actually update it every week.

-

Cash-planning app next. Better when you want visibility and routine without maintaining formulas or multiple tabs.

-

Full accounting stack later. Worth it when bookkeeping, reporting, and tax complexity justify the overhead.

If invoicing and collections are the real bottleneck, start with the tool comparison in Cash Flow for Freelancers.

Example: what this looks like after 2 weeks

In two weeks, the goal is not to become a finance person. It is process adoption: getting to the point where you have numbers you trust and a habit you can keep.

(Note: The following is a composite example based on typical solopreneur patterns.)

Before: Alex, a solo consultant, had one checking account. No forecast. No real split between operating cash, tax cash, and owner pay. Taxes were treated as a future problem.

After (Week 2): Subaccounts are active. A simple 13-week forecast exists, even if it is rough. Alex has a weekly calendar block. The Taxes + Reserve bucket has a real balance. Alex knows the next tight week before it arrives and what portion of the bank balance is actually safe to use.

Your under-1-hour implementation plan

You can set this up in one focused hour. No special tools required. Just a bank account, a browser, and a timer.

The setup checklist

- Open or label 3 subaccounts. Operating, Taxes + Reserve, Owner Pay (

10min). - Set up auto-transfer rules. Percentage split on deposit (

5min). - Identify recurring expenses. Export the last

3months of bank transactions (5min). - Start the forecast. Map out Week 1 beginning cash (

10min). - List open invoices. Client, amount, due date (

5min). - List upcoming bills. Everything due in the next

30days (5min). - Calculate safe-to-spend. Cleared operating cash minus near-term payables, tax gap, and protected buffer (

5min). - Schedule the review. Book a recurring calendar event (

2min).

Run the system without the spreadsheet

The three-bucket split, the weekly dashboard, and the safe-to-spend number all work in a spreadsheet — until the spreadsheet stops getting updated. onbalance keeps the same structure with less friction: see your forward balance, track obligations, and update in minutes from any device. No bank sync, no formulas to maintain.

Your data stays encrypted on your device. The architecture is detailed in the onbalance whitepaper.

Get started with onbalance — available on the App Store and Google Play.

FAQ: cash flow for solopreneurs

How much cash should a solopreneur keep in the bank?

Hold an absolute minimum of 3 weeks of mandatory cash outflows to survive a dry spell. If your income is volatile or you have client concentration, a 2 to 3 month reserve is a solid comfort target.

How can I improve cash flow with late-paying clients?

If late-paying clients are the main problem, switch to a collections playbook rather than adding more bucket rules. Use Cash Flow for Freelancers for deposits, milestone billing, reminder cadence, and contract-level fixes.

How do I set a safe-to-spend number?

Safe-to-spend = Cleared operating cash − Mandatory near-term payables − Tax funding gap − Protected buffer. Use conservative inflow assumptions for late payers.

How often should I adjust my bucket percentages?

Review after 4 to 6 weeks of real data, then quarterly. If your margins, fixed costs, or tax rate change materially, recalculate. Do not adjust based on a single good or bad month.

Should I keep taxes in the same bank as my operating cash?

No. Use a separate tax savings account to prevent accidental spending. Fund it automatically as a percentage of every client payment.

I have one large client. How do I reduce cash flow risk?

Increase your target reserve runway while the concentration exists. Shorten payment terms, align your largest recurring bills after the client's typical payment date, and build a pipeline to diversify inflows.

Do I count a business credit card as cash on hand?

No. Cash on hand means cleared cash. Credit can bridge timing, but it increases fixed obligations. Never count credit limits as liquidity.

Final thoughts

Most cash flow anxiety comes from guessing. When you mix accounts, ignore taxes, and do not look ahead, every decision turns into "I hope this is fine."

You do not need a finance degree. You need clarity. Separate the money, run the bucket split, keep a simple forecast, and spend 20 minutes every Monday updating it. Do it for two weeks and you will have a safe-to-spend number you actually trust.

This content is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified professional for guidance specific to your situation.

Cash flow tracking & future balance forecast with offline-first sync.

Get Started with onbalance