What Is a Cash Flow Forecast? Methods, Models & Mistakes

A cash flow forecast is a forward-looking estimate of cash inflows and outflows over time. It focuses on bank reality: what will clear, on what date, and what your balance will be after each movement. That is why a business can look profitable in the P&L and still end up short on payroll, taxes, or rent.

The 30-Second Brief (TL;DR)

- Profit is not cash. You can show accounting profit and still miss payroll.

- The goal. A cash flow forecast predicts when money will actually enter and leave your account.

- The method. For most small businesses, start with a direct 13-week rolling forecast.

- The trap. Do not confuse invoiced sales with collected cash.

- The discipline. Update weekly, compare forecast vs. actual, and adjust assumptions fast.

What a cash flow forecast actually tells you

The practical difference is timing.

A cash flow forecast makes that timing gap visible before it becomes a crisis. It shows what will clear, when it will clear, and what your bank balance will look like after each movement.

This is why many founders get surprised. Revenue can look strong in the P&L while cash remains tight because customers pay late and obligations are due now.

In the Federal Reserve's Small Business Credit Survey, 51% of employer firms reported uneven cash flow as a financial challenge.

Note: SBCS results come from a nationwide convenience sample, not a random sample.

Cash flow forecast vs. budget vs. P&L

Three tools. Three different jobs.

| Tool | What It Does | Time Orientation |

|---|---|---|

| Profit & Loss (P&L) | Measures profitability (revenue - expenses) | Past period view |

| Budget | Sets planned income and costs | Future (usually fixed) |

| Cash Flow Forecast | Predicts bank balance by date | Future (rolling, dynamic) |

If your question is, "Can I pay taxes and payroll on time?", the forecast is the primary tool.

A cash flow forecast is also different from the statement of cash flows: the statement shows where cash went in a past period, while the forecast shows whether you are likely to run short later.

The practical example: anatomy of a cash crunch

To understand why this matters, here is a common service-business scenario:

The situation:

- Oct 1. You finish a project and invoice $20,000.

- Oct 1. Under accrual accounting, the P&L recognizes $20,000 of revenue.

- Oct 15. Payroll of $15,000 is due.

- Nov 1. The client pays under Net 30 terms.

Without a forecast: You see revenue and assume you are safe. On Oct 14, cash has not arrived, and payroll risk appears too late.

With a forecast: The inflow is placed in November, not October. The model shows a deficit on Oct 15 weeks in advance.

Action: Delay a non-essential expense, negotiate partial prepayment, or arrange short-term coverage.

Why businesses need cash flow planning

The purpose of cash flow planning

Cash flow planning has one core job: keep the business liquid.

In practice, it supports three decisions:

- Liquidity protection. Spot shortfalls early.

- Capital allocation. Decide when to reinvest, build reserves, or reduce debt.

- Financing readiness. Show lenders and investors a credible repayment path.

Who should conduct cash flow planning?

Short answer: every business. Highest-risk groups include:

Small businesses account for 99.9% of U.S. businesses.

Forecasting discipline is not a niche finance practice. It is an operating necessity.

If your business faces payroll, inventory, and supplier timing gaps, use Cash Flow Forecasting for Small Businesses as your operating playbook. One-person businesses usually need a narrower approach: use Cash Flow for Solopreneurs when owner pay, taxes, and reserves are the main issue, or Cash Flow for Freelancers when invoice timing, deposits, and collections are the main bottleneck.

What data goes into a cash flow forecast

A forecast is only as good as its inputs.

Before opening a spreadsheet or app, gather:

Two metrics deserve regular monitoring: Operating Cash Flow (OCF) and DSO (Days Sales Outstanding), which tells you how long it takes to collect invoices. For the formulas and context behind these and other cash flow metrics, keep the Cash Flow Glossary open alongside this guide.

Direct vs. indirect forecasting methods

There are two core methods: the direct method and the indirect method. Forecasting borrows the same logic.

| Feature | Direct Method | Indirect Method |

|---|---|---|

| Basis | Expected receipts and payments by date | Projected profit adjusted for non-cash items + working capital timing |

| Typical horizon in practice | Near-term operations (often 13-week rolling) | Longer-term planning (monthly/quarterly) |

| Strength | High timing accuracy | Strategic trend visibility |

| Best use case | Liquidity control and early warning | Annual planning and financing narrative |

Recommendation: Start with a direct 13-week rolling forecast, then add an indirect model for longer horizons.

| Business situation | Horizon and method | Update cadence | Why it fits |

|---|---|---|---|

| Tight weekly cash timing | Direct 13-week rolling forecast | Weekly | Best for payroll, rent, tax dates, and short-term collection risk |

| Strategic planning or lender conversations | Indirect 12-18 month forecast | Monthly | Better for trend visibility and financing narratives |

| High-growth or seasonal periods | Direct 13-week forecast plus short-term in-period checks | Weekly, with extra monitoring during peak periods | Volatility makes monthly-only visibility too slow |

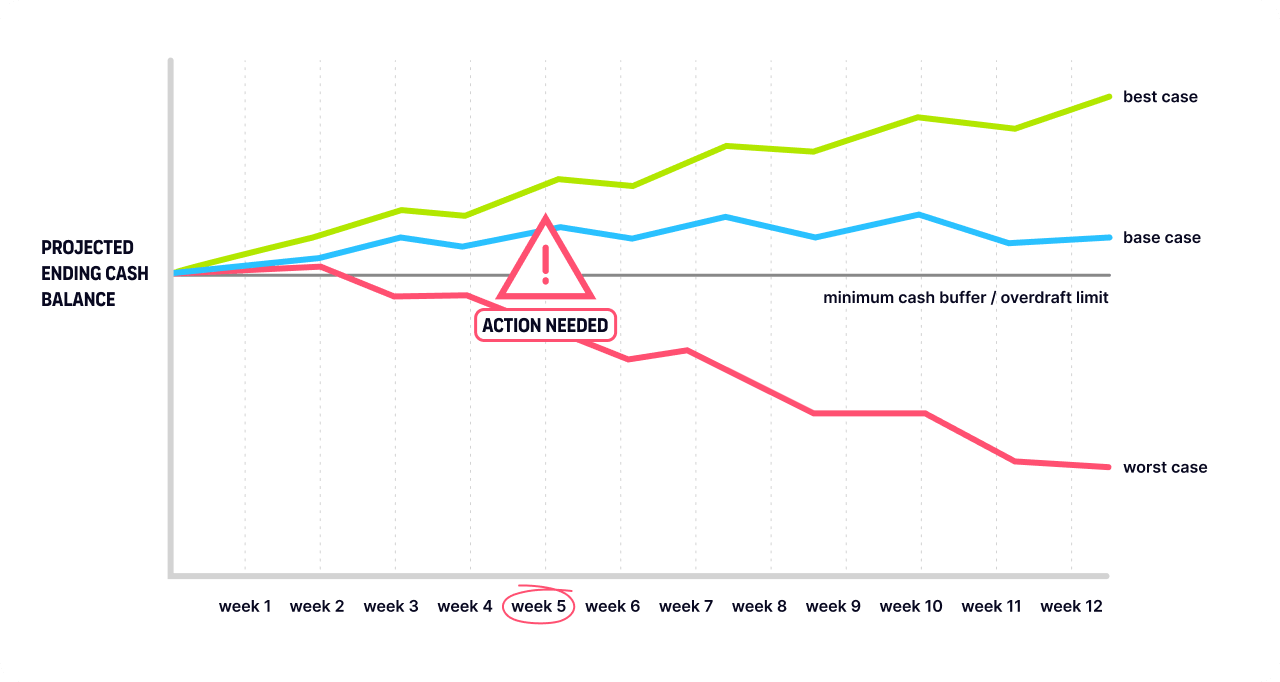

Scenario planning for "what if" cases

One forecast reflects one set of assumptions. Scenario planning gives you options.

Build three versions:

- Base Case: most likely.

- Best Case: faster collections, stronger sales.

- Worst Case: delayed payments, lower demand.

Then define trigger points:

-

At what date does the balance cross your safety floor?

-

Which expense can be delayed first?

-

Which commercial action, such as a deposit, revised terms, or a credit line, is activated?

Caption: A good scenario chart shows the exact week the downside case breaks the safety floor, not just that risk exists.

Variance analysis: why your forecast was wrong

Every forecast will be wrong. The objective is to be wrong for known reasons.

Run a weekly variance loop:

- 1

Lock weekly forecast assumptions

Freeze the week's expected collections, payments, and timing assumptions.

- 2

Import actual bank movements

Pull in what actually cleared.

- 3

Measure variances by customer, vendor, and category

Compare each line item against the forecast.

- 4

Label the root cause

Classify the gap as a timing shift, amount error, missing line item, or one-off event.

- 5

Update assumptions for the next cycle

Use the variance review to improve the next weekly forecast.

This is how forecasts become a practical weekly management tool instead of a one-time spreadsheet.

5 common cash flow forecasting mistakes

1. Confusing revenue with cash

An invoice is not cash. Put receivables in your base case only with realistic payment dates. Move uncertain items into scenarios, or weight them.

2. Relying on manual methods without controls

Spreadsheets are flexible but fragile. If you stay manual, implement version control and an assumptions log. If you automate, prioritize auditability and data privacy. For founders who need a lightweight, privacy-first setup, tools like onbalance focus on local data control and full offline access.

3. Ignoring seasonality and lump-sum outflows

Annual insurance, tax deadlines, and renewals should be forecast on exact dates, not averaged monthly.

4. Over-optimistic receivables assumptions

Do not hardcode Net 30 if your reality is Net 45 or Net 60. Payment timing shifts with customer behavior and the economy.

Xero Small Business Insights tracks "time to be paid" and "late payments" for U.S. small businesses.

5. Ignoring red flags in the model

A forecast is useful only if it triggers decisions. Key red flags include recurring negative operating cash, rising DSO, and debt-funded routine expenses.

Choosing a cash flow forecasting tool

The right tool depends on business complexity, update cadence, and privacy requirements.

For larger finance teams

-

Often need bank connectivity, multi-entity support, and treasury workflows.

-

Typical options include platforms like Cobase, Agicap, Fathom, and PlanGuru.

For small businesses and solo founders

-

Simplicity and consistency usually matter more than broad integrations.

-

A practical stack should let you capture inflows and outflows fast, update weekly, and keep assumptions visible.

-

onbalance is built for this use case: weekly cash planning with end-to-end encryption, no bank sync required, and offline access.

FAQ on cash flow forecasting

What is included in a cash flow forecast?

At minimum, a forecast needs starting cash, money expected in, money expected out, and the closing balance for each period. For most small businesses, that means customer collections, payroll, rent, taxes, supplier payments, debt payments, and occasional items like owner draws or equipment purchases.

How do you calculate a cash flow forecast?

On paper, it is simple: opening cash + expected receipts - expected payments = ending cash. The hard part is not the math. It is getting the timing right. In small-business usage, cash flow projection usually means the same thing as cash flow forecast.

Should I use a daily, weekly, or monthly cash flow forecast?

Weekly is the default for most businesses. Move to daily only if cash is tight or a lender wants that level of reporting. Monthly works for longer-range planning, but on its own it is often too blunt for near-term cash decisions.

Why do many businesses use a 13-week cash flow forecast?

Because 13 weeks is one quarter. That is long enough to capture payroll runs, tax dates, supplier terms, and slow collections without drifting too far into guesswork. It is the standard short-term model because it is detailed enough to drive real decisions.

What level of accuracy is realistic?

The first 1-4 weeks should usually be tighter because many items already have dates and amounts attached to them. Later weeks get fuzzier. You are not trying to predict the future perfectly. You are trying to spot a cash gap early enough to do something about it.

Is a template enough to start?

Yes. For most small businesses, a simple template is enough to get started. What matters is that you keep it current, use realistic collection dates, and compare forecast vs. actual every cycle. If you want a starting point, use a 13-week cash flow forecast template.

The bottom line

Cash flow forecasting is not about perfect prediction. It is about reducing operational risk.

When you know your expected bank balance by week, decisions become proactive instead of reactive. You may still see deficits, but you see them early enough to act.

Start simple. Update consistently. Treat the forecast as a living operating tool.

This content is for informational purposes only and does not constitute financial, tax, or investment advice. Consult a qualified professional for guidance specific to your situation.

Cash flow tracking & future balance forecast with offline-first sync.

Get Started with onbalance